Bank Account Changes

One of the key components in managing your money will most likely be your checking & savings accounts. As simple as your accounts may be, though, the discussion about whether to mix them in common pots or keep them separate may not seem as simple. Take a look below for benefits on both sides of that aisle.

To join or not to join. That is the question. Both methods have their own benefits, & some benefits may weigh more heavily for you than others. If you're debating whether you want to join all your money into one account or keep your assets separate, consider that you may even be able to use a combination of both accounts effectively.

To join or not to join. That is the question. Both methods have their own benefits, & some benefits may weigh more heavily for you than others. If you're debating whether you want to join all your money into one account or keep your assets separate, consider that you may even be able to use a combination of both accounts effectively.

Joint Accounts:

By taking a mixed approach to joint and individual account, your joint accounts would cover--well, joint expenses. That would be rent/mortgage payments, groceries, utilities & other common expenses. Either spouse has access to these accounts in order to make the payments.

If you were to decide on keeping all of your money in joint accounts, understand that you will also need to flexible with one another on individual expenses like hobbies also coming out of the account.

Individual Accounts

Individual accounts in a mixed approach allow each spouse a portion (percentage or set amount) of the income for individual expenses such as hobbies, clothes, and phones. The individual responsibility of the separate account places a certain level of trust on each spouse to manage his or her money wisely, & that responsibility will hopefully carry over to the joint account. Moreover, separate accounts can provide a safety net in case one spouse's account or the joint account is compromised.

The Right Balance

Whatever your balance of joint and separate accounts, be open and regularly talk about your account information. Separate accounts should never be used for financial secrecy (surprise gifts excluded). Take a candid approach to help you stay accountable. That's what you have each other there for after all.

If you do decide to set up a joint account, you'll need some basic information to get started with the process. Take a look below for answers to some common set-up questions along with some account management tips.

Account Setup

How do we merge accounts?

Merging Accounts can be done easily with a switch kit like this one. Once you complete the switch kit for your bank, take it to your banker who can start the process of moving the necessary accounts.

As a general note to changing account information (including all the following questions), all involved parties need to be present.

What do we need in order to merge accounts?

You need to bring a primary form of ID (such as a passport or driver's license), social security number & any basic account information. Your banker will have the forms you need for consolidating your money.

When should you merge accounts?

Don't feel like this is one of those steps to lump between finding a dress & saying your vows. If you're not sharing expenses before the wedding, then there's no real advantage to combining expenses until after the wedding. If you're concerned about starting to build accountability around your money, then you need to start talking about your finances with one another rather than combining them.

How do you remove parents from an account?

In most cases, with all parties on the account there at the bank, you will only need to complete a name release notification provided by your banker. Be aware, however, that some financial institutions may not allow you to remove a parent from the account without closing the account altogether. Contact your banker if you have questions on your bank's specific policy.

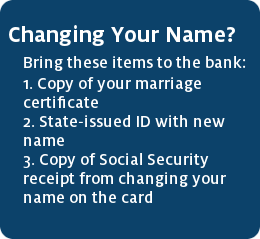

How do you change a name on your account?

If you have changed your legal name & need to make this adjustment on your accounts as well, bring the bank a copy of your marriage certificate, a copy of the social security receipt from when your name was changed & a state-issued ID showing your new name. This, of course, means that you will need to take care of these other steps before you adjust the information on your bank account. Contact your banker if you have specific questions about this process.

If you have changed your legal name & need to make this adjustment on your accounts as well, bring the bank a copy of your marriage certificate, a copy of the social security receipt from when your name was changed & a state-issued ID showing your new name. This, of course, means that you will need to take care of these other steps before you adjust the information on your bank account. Contact your banker if you have specific questions about this process.

Account Maintenance

Should one or both of us keep the register?

You register is the account log of withdrawals, deposits, transfers & interest that you keep along with your checkbook. And yes, you should keep track of it, even if you have online banking & statements as well. Automated systems can mess up sometimes, & it's good to have another record on hand to compare with.

As to both of you keeping the record, too many cooks in the kitchen is never a good thing. Rather than both people having a direct hand in maintaining the register, it might be better for one of you to report your transactions to the other & then talk through the register together at set times.

As to both of you keeping the record, too many cooks in the kitchen is never a good thing. Rather than both people having a direct hand in maintaining the register, it might be better for one of you to report your transactions to the other & then talk through the register together at set times.

This doesn't negate the responsibility of either person, though. When either person slacks in his/her part of the records, the potential for errors greatly increases & could even lead to lapses in payments with one spouse ruining the credit of the other. Both individuals need to take initiative in maintaining finances, even if it's in different roles.

Should we use direct deposit?

And should we automatically split deposits for our direct deposit?

If you have the option for direct deposit through your employer, use it. Most employers offer it as a payroll option; it's free to employees; & it may even allow you to waive the checking account fee at your bank. Electronically depositing your income into your account or accounts is secure & much faster than waiting to get a payment in the mail & then taking it or sending it to the bank for deposit.

Automatically depositing portions of your income to different accounts makes your money management even easier than directly depositing into one account, too. Consider it. It's no cost to set up a split, & you can make designations by percentage or fixed amount. Past studies by NACHA, the National Automated Clearing House Association, have also shown that couples who automatically split their deposits between checking & savings accounts end up saving more money per month than couples who send everything to one account. You will just need to nail down your monthly budget so you know how much to allocate in each direction. Also, check with your financial institution about the number of accounts you can split between.